The Rapid Payments Programme is bringing a change to instant payments in South Africa. Let’s have a look at what this means, and why it is needed.

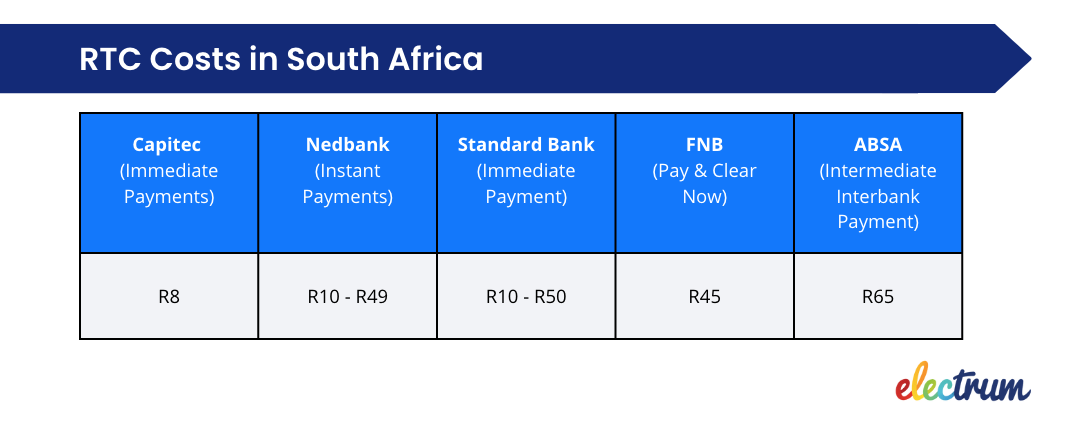

As South Africans, we are often frustrated by the limited options for immediately transferring money to people at different banks to ours. Regular transfers can take up to two business days, which, in this time of immediate gratification can be a real inconvenience. Not to mention the anxiety of making an error when manually inputting the banking details. If a mistake is made, you have no way of knowing about it until the recipient awkwardly asks about the payment. Requesting an immediate payment is really expensive in South Africa, as illustrated here:

South Africa was one of the first countries to implement instant payments back in 2006. Built for the instant clearing of high value, low volume transactions, the South African RTC (real-time clearing) system processes transactions within 60 seconds using a message process, and a message protocol that's been unchanged for over 20 years. RTC transaction volumes amount to only 3% of all EFT transactions - indicating to us that a better, safer, more cost-effective system is desperately needed. This is where RPP will play a crucial role.

Will RPP solve our instant payment pain?

In 2018 BankservAfrica embarked on their Rapid Payments Programme (RPP) to define a mobile-friendly instant payment platform for the industry. This programme will address key needs identified both in the Vision 2025 and Project Future recommendations: increasing financial inclusion, reducing South Africa’s dependency on cash, and creating an integrated platform for payments.

RPP differs fundamentally from RTC by making use of modernised payment rails and message protocols; creating an environment where low value, high volume transactions can become faster and more cost-effective. The capability of RPP includes:

-

Sending instant payments with the ability for the recipient to receive and use the funds immediately, no matter which bank they are with.

-

The ability to access payments in a simpler way, by using identifiers such as an email address or phone number.

-

The ability to easily request a payment from someone through a feature called ‘Request to Pay’.

What South Africa can learn from India and Thailand

This type of system is already working well in other parts of the world. India’s Universal Payments Interface (UPI) introduced in 2016 was fuelled by a demonetisation goal to curb corruption. By combining the accessible and widespread national identity base (Aadhaar) with their real-time payments service (IMPS), UPI was released.

UPI was initially used to offer a government-sponsored mobile service, but it really took off once it was used to enable payments within a range of third-party social apps such as PayTM, Google Pay, and WhatsApp Pay.

In Thailand, PromptPay enables users to make and receive payments into their bank accounts or into digital wallets linked to their national ID, mobile phone numbers, or email addresses. By designing PromptPay to support the use of personal identifiers as proxies for a person’s account or digital wallet, everyone, including the unbanked, is now able to make and receive free digital and contactless payments.

Adopted by all the major banks in Thailand, PromptPay has been transformational. Since its launch, it has attracted 43 million users and processed more than 765 million transactions. As a result, PromptPay has connected a nation that previously suffered from geographical and cultural issues when it came to paying friends, family, salaries, and business invoices. It is easy to make correlations to South Africa. Now, in Thailand, free digital and contactless payments are available to everyone, revolutionising how the country transacts between people and businesses.

Transforming digital payments

We can see why free or low-cost digital payments are so desperately needed here in South Africa. Our reliance on cash is expensive - with users suffering from fees, losing out on interest, spending time in queues, or travelling to find ATMs or bank branches. Not to mention the safety risks of carrying and storing cash.

We believe that RPP is poised to transform the way South Africans view and use digital payments, ultimately contributing to financial inclusion across the country. Get ready for what RPP will bring and start exploring how you can build a modernised payments business.

Chat to us today to see how Electrum can help.