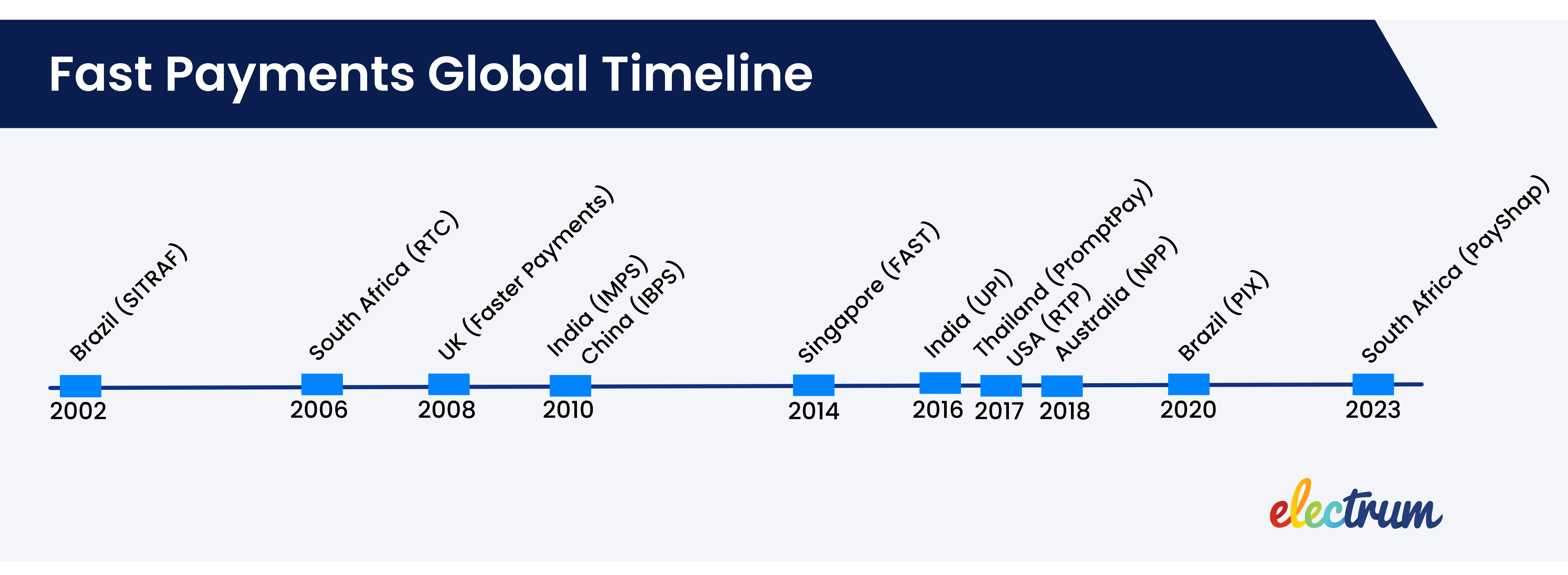

Fast payment systems have revolutionised the way we conduct financial transactions. By definition, these payments make funds available within seconds and are available as close to 24/7/365 as possible. Let’s take a look at seven case studies of fast payment systems from around the world.

South Africa has two notable fast payment systems: RTC (real-time clearing) was introduced in 2006, while PayShap had its initial roll-out in March of this year. Electrum’s recent research into payments modernisation has highlighted that South Africa can continue to learn from these international successes and implementations.

Globally, fast payment systems have gained significant popularity, with more than 70 countries adopting various forms of them. In this summary, a few selected examples that are relevant to South Africa are highlighted and explored. The countries selected include those examined in the ‘Payments Study Tour’ embarked on by SA industry delegates in 2019, as well as countries which were identified by industry experts during payments research conducted by Electrum.

Country Case Studies

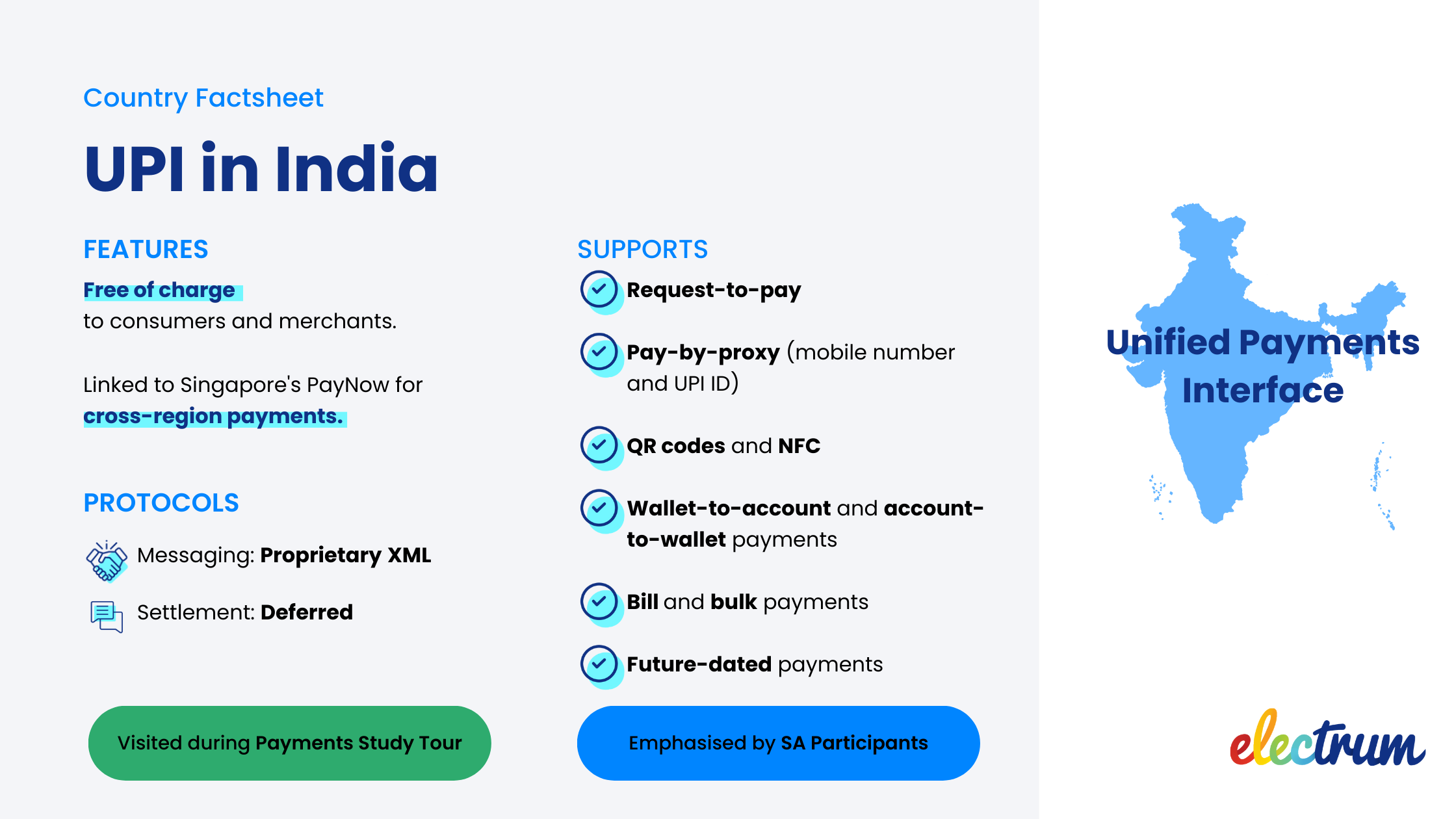

India

To drive the adoption of the Unified Payments Interface (UPI) the Indian government launched their Bharat Interface for Money (BHIM) payments app. BHIM served to showcase UPI’s capabilities and the government offered cash incentives to both merchants and consumers for adopting UPI payments.

India’s fast payments systems have seen massive success - they are the biggest fast payments market with 46.8 billion fast payment transactions in 2021 alone. This success is inspiring to participants in the South African payment processing industry. UPI is regarded as a ‘poster child’ thanks to its achievements in driving consumer adoption and reducing cash. Given the similarities between South Africa and India in terms of market dynamics and a large informal traders’ market, there is optimism that South Africa can replicate India’s success with its own fast payment system.

Singapore

Singapore is an interesting example of a country that added support for proxy-based payments via an overlay service instead of through core Fast and Secure Transfers (FAST) functionality. Moreover, the proxy overlay, PayNow, is owned by a separate entity from the owner and operator of FAST.

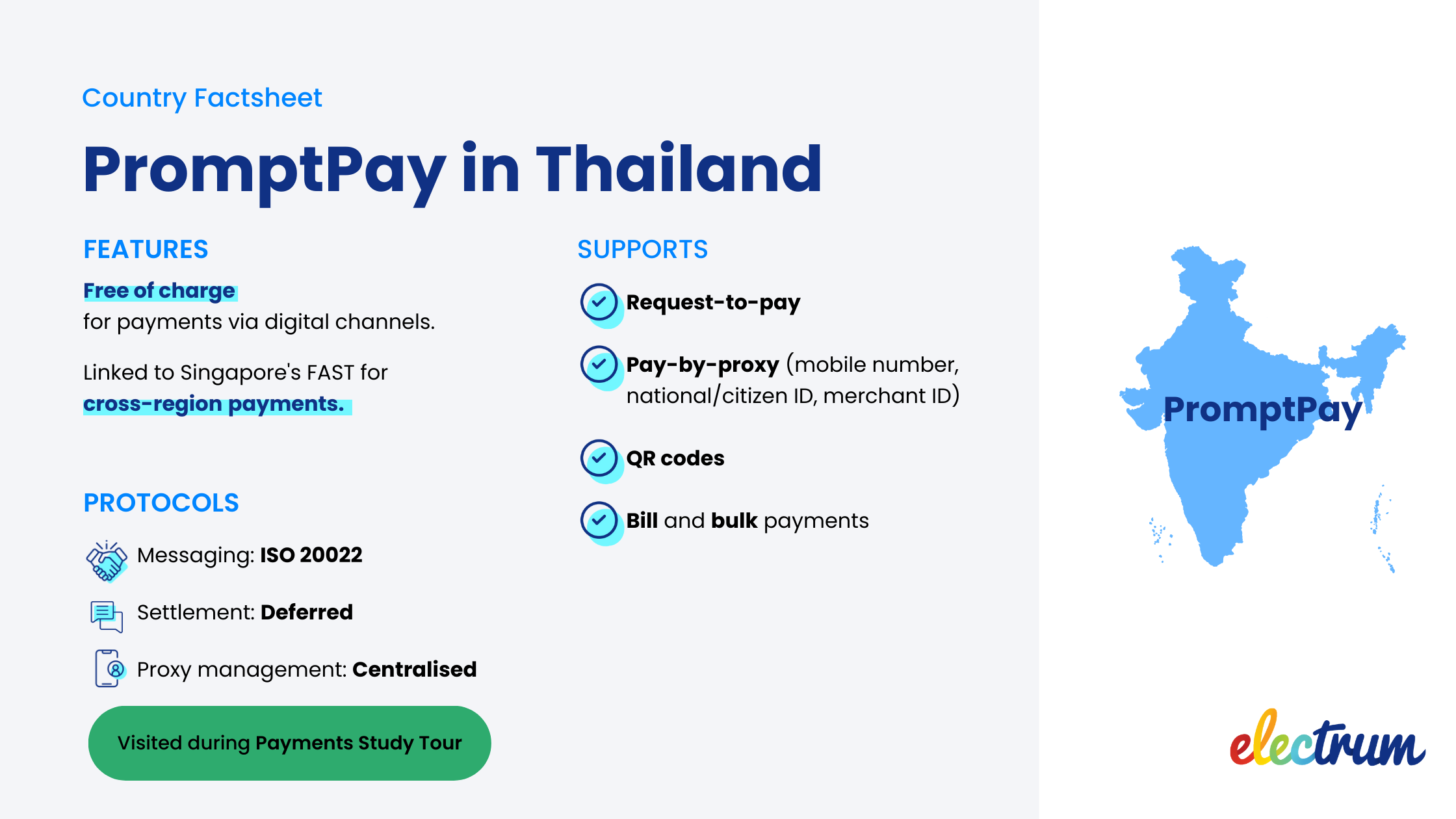

Thailand

PromptPay went live in 2017 and supports a large set of significant use cases (as shown in the image above).

After the launch of standardised Thai QR codes, support for QR code payment was enabled by launching MyPromptQR in September 2019

China

China has implemented several notable security measures for their Internet Bank Payment System (IBPS): (1) For proxy registration, a bank account must be open for at least 6 months; (2) a registered mobile number must be in use for at least 6 months before it can be used as a proxy; (3) during proxy registration, two dynamic authentication factors must be used to validate the customer’s identity; and (4) for every payment through a proxy, IBPS performs an online validation of the beneficiary corresponding to the proxy.

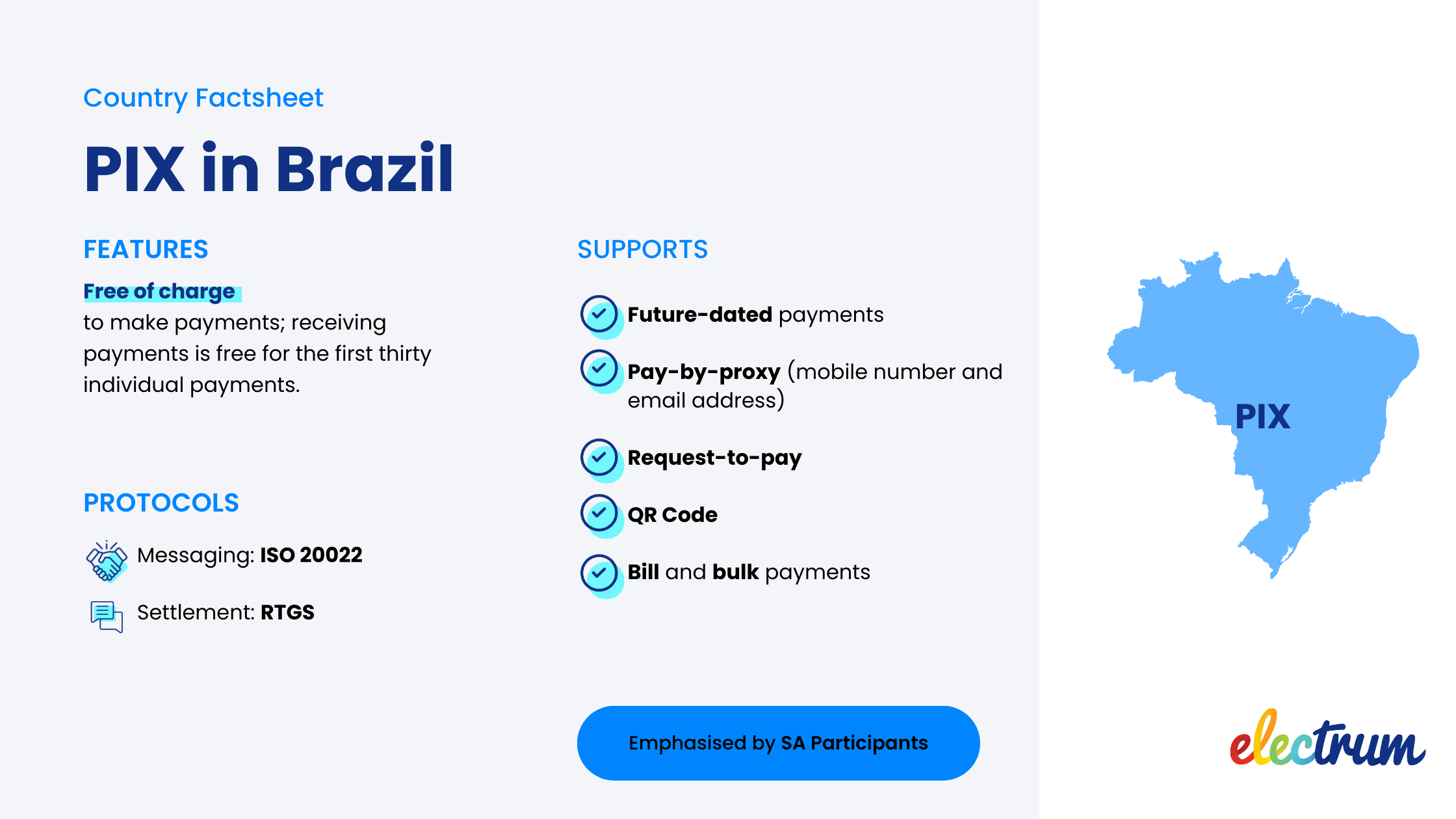

Brazil

SITRAF (Sistema de Transferência de Fundos) was one of the earliest fast payment systems, launched in 2002. It made use of a proprietary message protocol and had very limited use case capability. This was followed by the Pix in 2020.

Similar to India’s UPI, payment participants in South Africa have a very high regard for Pix and are hoping to make use of several learnings from Brazil’s approach. Examples of this approach include ensuring a uniformity of integration based on a very clear integration specification that allows participants to easily join and process on the Pix rail. Also, Pix has a very well-articulated model describing the future view of the open financial industry.

An interesting attribute of Pix is users’ ability to manage payment limits, with a waiting time of 24 hours for a limit change to take effect.

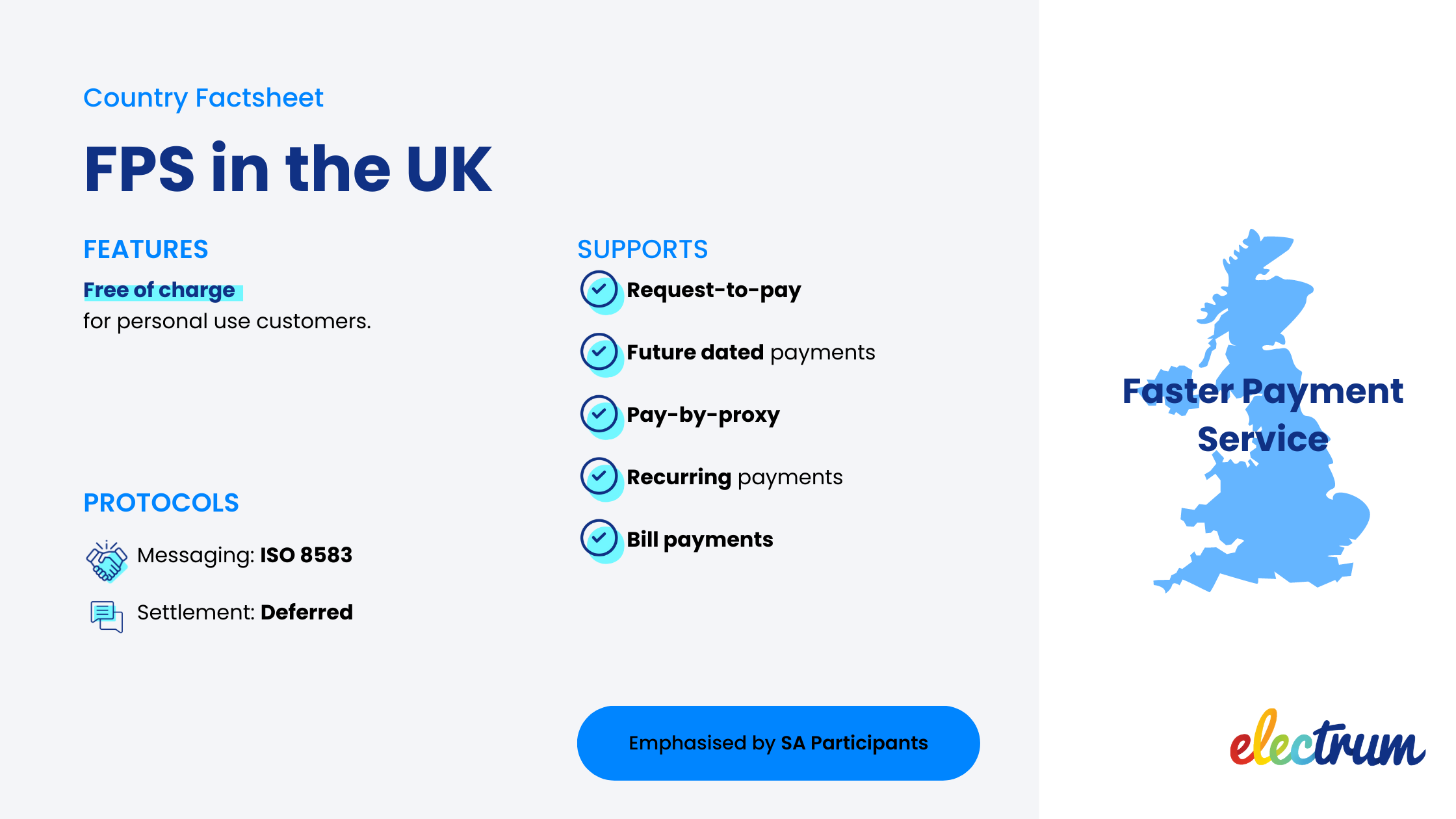

United Kingdom

The UK’s FPS (Faster Payment Service) became available in 2008. Though being one of very few fast payment systems that is still based on ISO 8583 messaging standards, it is able to support a variety of important use cases.

European Union

The European Union has established the Single Euro Payments Area Credit Transfer (SCT Inst) to enable fast payments across participating countries. The solution is based on a number of pan-European as well as regional clearing and settlement providers (CSMs) that are available for facilitating these payments via funds held at the European Central Bank. Any payment provider wanting to participate in SCT Inst needs to be a member of at least one of these clearing and settlement providers.

Functionality of Fast Payments

When exploring fast payment systems of these countries, the following questions shed light on their functionality and effectiveness:

1. What use cases are supported?

While person-to-person (P2P) and person-to-business (P2B) payments are generally supported, other use cases such as request-to-pay have gained importance, and some systems enable innovative features such as future-dated payments.

2. Is the system based on ISO 8583 or ISO 20022 messaging standard?

ISO 8583 is still used by some countries due to the high cost and complexity of upgrading to ISO 20022, but the latter is generally preferred by many countries thanks to its rich data support, flexibility, and level of control over message content and structure. However, a few countries use neither ISO 8583 nor ISO 20022 but prefer a proprietary protocol instead that offers more flexibility than ISO 20022.

3. Can consumers pay with proxies instead of using beneficiary account information? What proxies are supported, and how is it accomplished?

Proxy management can either be via a centralised system that manages and resolves proxies for all participants, or it can be decentralised so that each bank manages its own users’ proxies and is responsible to resolve them at the time of a transaction. Some countries even outsource proxy management as overlay services to a third party.

4. Are fast payments free of charge to consumers, or did the government leave it to the banks and service providers to determine fees?

This has an impact on consumer adoption and overall success of the initiative.

5. Are transactions settled in real-time through (most likely, pre-funded) real-time gross settlement (RTGS), or is there an approach of deferred net settlement?

Deferred net settlement (DNS), where inter-participant obligations are settled on a net basis at the end of predefined cycles during each day, conveniently reduces liquidity needs for participants, but has an increased credit risk due to the build-up of participant debit positions. Some countries mitigate this risk by requiring sufficient pre-funding from participants or applying participant debit caps. RTGS ensures that all obligations are settled immediately, but has a high demand on participant liquidity.

Further Reading

For the information in this summary, Electrum has made use of the following resources:

-

Considerations and Lessons for the Development and Implementation of FAST PAYMENT SYSTEMS is a comprehensive report published by the World Bank Group in September 2021. This is a fascinating read and provides an incredible amount of information about payment systems in many countries - too much to mention in this study!

-

The World Bank also provides a Fast Payments Tracker that is useful as an easily-searchable and up-to-date reference on the most important characteristics and features of fast payment systems across the globe.

-

Mastercard published a blog in March 2023, Your real-time guide to real-time payments, that provides an insightful overview of some important general aspects of fast payments and highlights a number of interesting attributes of specific systems.

-

ACI Worldwide’s Prime Time for Real-Time Global Payments Report of April 2022 is an extensive study on fast payment systems across the globe.